Alternative Vehicles are Enabling a Secondary Market Revival

There's more to the story behind the secondary market's growth

Over the last five years, venture capital (VC) has seen remarkable growth, with approximately half a trillion dollars raised by VC funds, according to the National Venture Capital Association. Despite a record fundraising year in 2022, VC fundraising has since declined as interest rates have risen. Yet, due to differences in public and private market regulations, private company investments are expected to drive another wave of VC growth over the next decade.

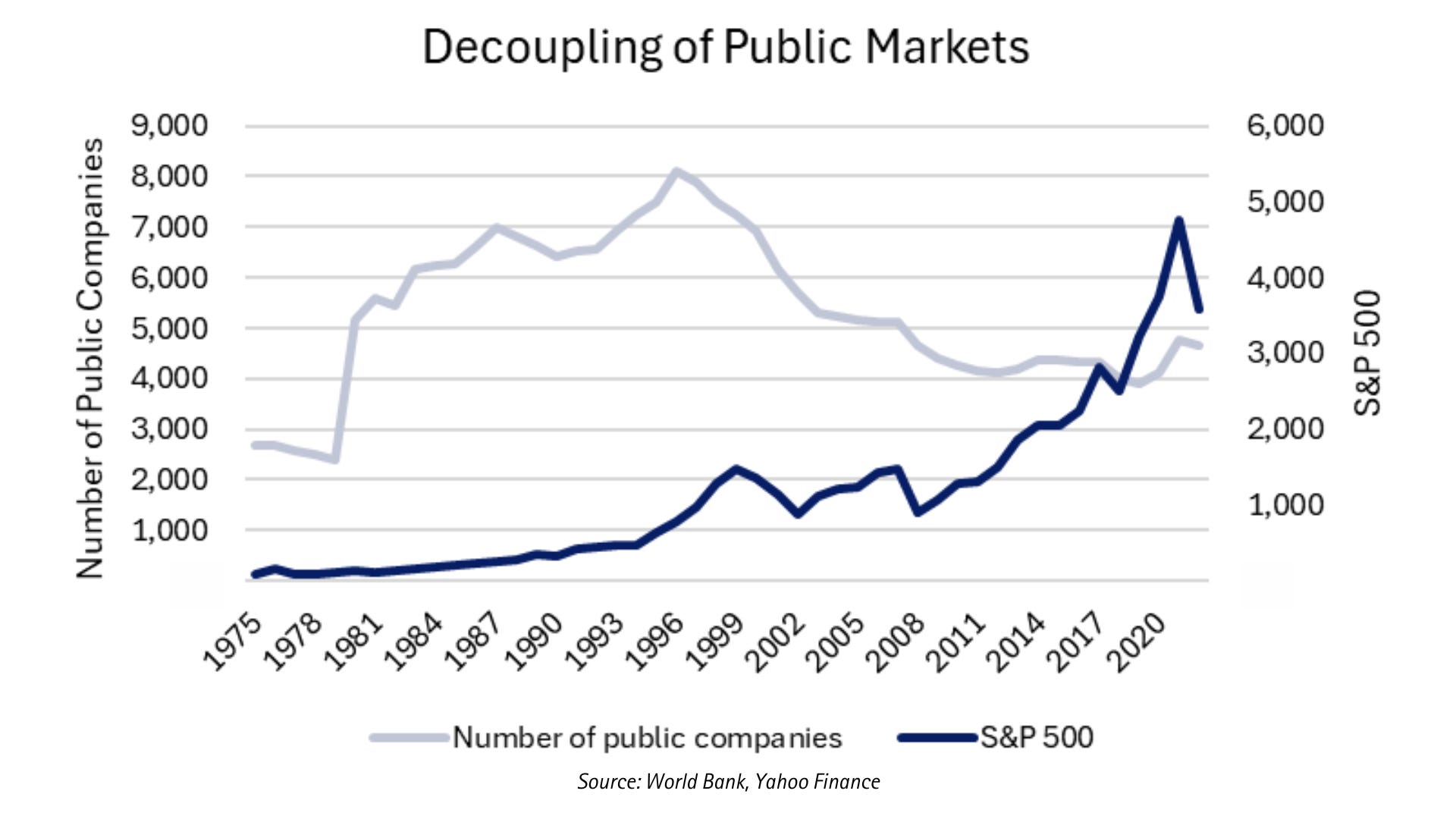

The National Securities Markets Improvement Act of 1996 simplified investment regulations, making it easier for alternative asset managers to raise funds. This shift prompted capital to flow into private markets, causing the number of public companies in the U.S. to decline. The 2002 Sarbanes-Oxley Act, with its stricter reporting and auditing standards, further discouraged companies from going public. As a result, companies are now taking longer to go public, and the number of public companies in the U.S. has halved since its 1996 peak. Without significant regulatory reform, many companies are likely to remain private, while public de-listings continue.

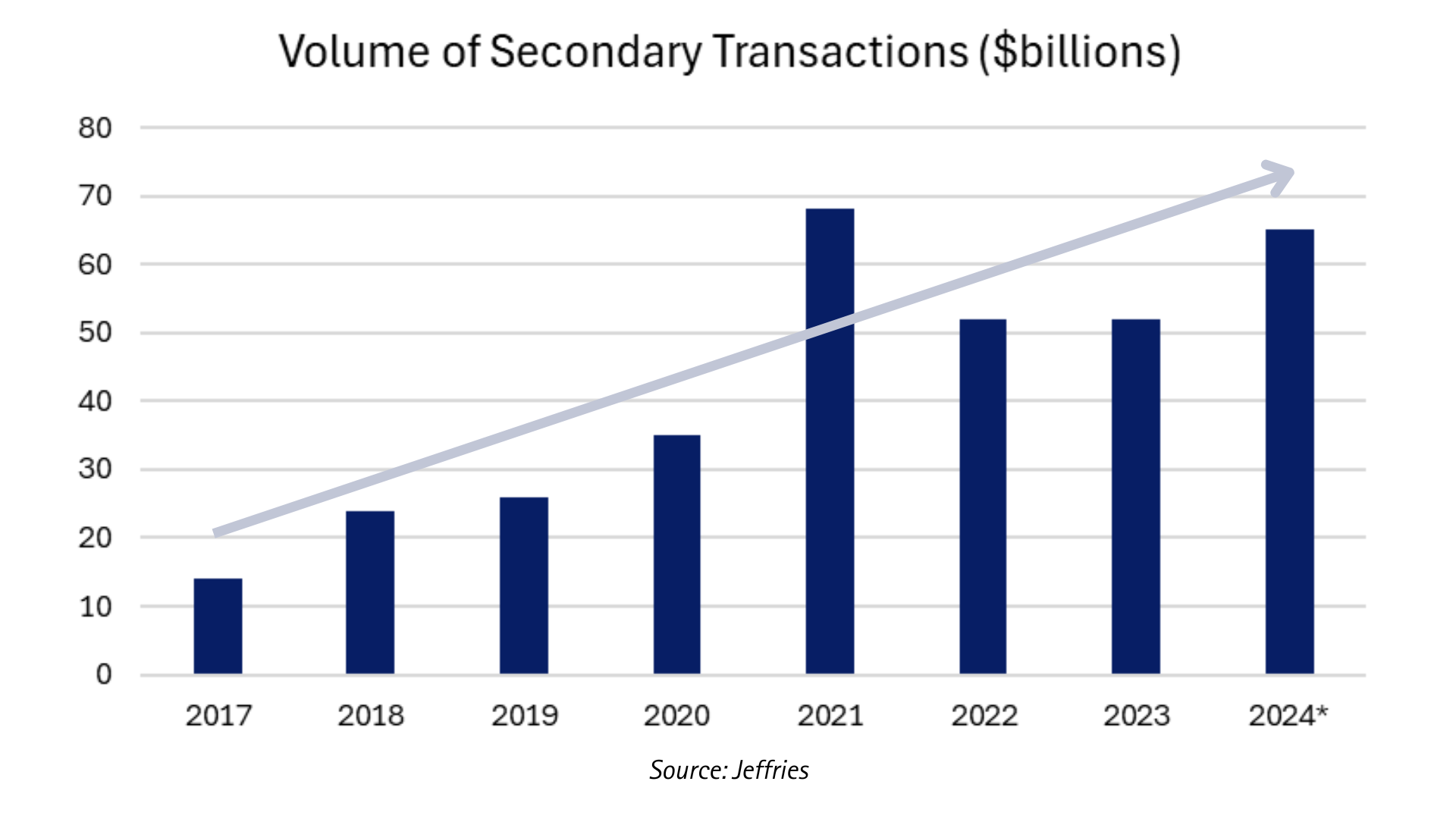

Capital markets have taken notice and adapted. Since 2017, the value of equity sales in private companies (known as secondary transactions) has grown nearly fivefold. By 2024, the total value of secondary transactions is projected to approach the 2021 record. As liquidity in secondary markets increases, the cost of capital continues to fall— a powerful trend capital allocators cannot afford to ignore.

Deploying capital into secondary markets is fundamentally different—financial information and company shares are often less accessible than in public markets. To navigate this, capital allocators partner with VC funds that have insights into portfolio companies' financials and share access. These allocators mirror VC strategy: investing in funds to establish toehold positions in early-stage companies, then doubling down on winners through direct share purchases in secondary markets.

While economic conditions may eventually shift, prompting more companies to list publicly, the secondary market has already proven to be a viable alternative for capital allocators.

VC will continue to lead the way.